Doprava zdarma se Zásilkovnou nad 1 299 Kč

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 64 Kč

Zásilkovna 44 Kč

PPL 99 Kč

Jak nakupovat

Jak nakupovat

Pomoc

Doručení

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 64 Kč

Zásilkovna 44 Kč

PPL 99 Kč

Doprava zdarma se Zásilkovnou nad 1 299 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

▸

Prázdný :-(

0

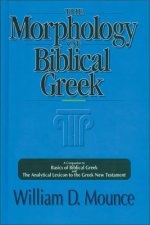

Credit Risk

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

This comprehensive and accessible introduction to modelling credit risk is tailored for master's stu...

Celý popis

Libristo kód: 01016755

?

129 b

129 b

129 b

1 285

Kč

Skladem u dodavatele

Odesíláme za 9-13 dnů

30 dní na vrácení zboží

Mohlo by vás také zajímat

/

Brožovaná

/

Brožovaná

451

Kč

451

Kč

/

Pevná

8 016

Kč

/

Pevná

8 016

Kč

This comprehensive and accessible introduction to modelling credit risk is tailored for master's students. It focuses on the two mainstream approaches, structural models and reduced form models, and on pricing selected credit risk derivatives. Balancing rigorous theory with financial intuition, it features detailed worked examples and exercises.

Informace o knize

Plný název

Credit Risk

Autor

CAPI SKI MAREK

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2016

Počet stran

201

EAN

9780521175753

ISBN

9780521175753

Libristo kód

01016755

Nakladatelství

Cambridge University Press

Váha

340

Rozměry

153 x 228 x 10