Doprava zdarma se Zásilkovnou nad 1 299 Kč

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 64 Kč

Zásilkovna 44 Kč

PPL 99 Kč

Jak nakupovat

Jak nakupovat

Pomoc

Doručení

PPL Parcel Shop 54 Kč

Balík do ruky 74 Kč

Balíkovna 49 Kč

GLS 54 Kč

Kurýr GLS 64 Kč

Zásilkovna 44 Kč

PPL 99 Kč

Doprava zdarma se Zásilkovnou nad 1 299 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

▸

Prázdný :-(

0

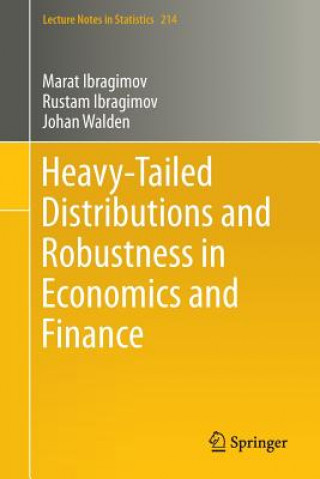

Heavy-Tailed Distributions and Robustness in Economics and Finance

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

This book focuses on general frameworks for modeling heavy-tailed distributions in economics, financ...

Celý popis

Libristo kód: 09215935

?

168 b

168 b

168 b

1 681

Kč

Skladem u dodavatele v malém množství

Odesíláme za 10-15 dnů

30 dní na vrácení zboží

Mohlo by vás také zajímat

/

Pevná

/

Pevná

1 681

Kč

1 681

Kč

This book focuses on general frameworks for modeling heavy-tailed distributions in economics, finance, econometrics, statistics, risk management and insurance. A central theme is that of (non-)robustness, i.e., the fact that the presence of heavy tails can either reinforce or reverse the implications of a number of models in these fields, depending on the degree of heavy-tailedness. These results motivate the development and applications of robust inference approaches under heavy tails, heterogeneity and dependence in observations. Several recently developed robust inference approaches are discussed and illustrated, together with applications.§

Informace o knize

Plný název

Heavy-Tailed Distributions and Robustness in Economics and Finance

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2015

Počet stran

119

EAN

9783319168760

ISBN

3319168762

Libristo kód

09215935

Nakladatelství

Springer International Publishing AG

Váha

2175

Rozměry

155 x 7 x 9