Doprava zdarma při nákupu nad 1 499 Kč přes Zásilkovnu nebo PPL Box.

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Kurýr DPD 69 Kč

PPL shop 49 Kč

Balíkovna 69 Kč

PPL kurýr 74 Kč

PPL box 39 Kč

Balíkovna 49 Kč

Výdejní místo DPD 49 Kč

Zásilkovna 39 Kč

Kontakt

Kontakt Jak nakupovat

Jak nakupovat

Pomoc

Doručení

Kurýr DPD 69 Kč

PPL shop 49 Kč

Balíkovna 69 Kč

PPL kurýr 74 Kč

PPL box 39 Kč

Balíkovna 49 Kč

Výdejní místo DPD 49 Kč

Zásilkovna 39 Kč

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

▸

Prázdný :-(

0

Doprava zdarma při nákupu nad 1 499 Kč přes Zásilkovnu nebo PPL Box.

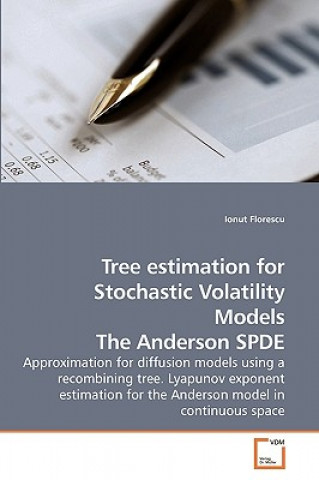

Tree estimation for Stochastic Volatility Models The Anderson SPDE

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

This text is divided into two parts. In the first part we present a methodology for approximating co...

Celý popis

Libristo kód: 06821528

?

121 b

121 b

121 b

1 209

Kč

U nakladatele na objednávku

Odesíláme za 17-27 dnů

Až 30 dní na vrácení zboží

Zákazníci také koupili

/

/

Brožovaná

Brožovaná

643

Kč

643

Kč

This text is divided into two parts. In the first part we present a methodology for approximating complex stochastic processes. Furthermore, we present an application to finance to calculate the price of American or European options when the price of the underlying equity obeys these complex processes. In the second part we investigate the exponential behavior of the solution of the parabolic Anderson model when the time goes to infinity. We show that the relevant quantity (the Lyapunov exponent) exists, and we provide tight lower and upper bounds for it.

Herečka

&

Polyglotka

EWA KASP

pro

Přehrát video

Libristo má největší výběr cizojazyčné literatury. Proto své knihy kupuji tady.

Informace o knize

Plný název

Tree estimation for Stochastic Volatility Models The Anderson SPDE

Autor

Ionut Florescu

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2010

Počet stran

116

EAN

9783639127669

ISBN

3639127668

Libristo kód

06821528

Nakladatelství

VDM Verlag

Váha

181

Rozměry

152 x 229 x 7

Kategorie

Darujte tuto knihu ještě dnes

Je to snadné

1 Přidejte knihu do košíku a zvolte doručit jako dárek 2 Obratem vám zašleme poukaz 3 Kniha dorazí na adresu obdarovanéhoMohlo by vás také zajímat

/

Brožovaná

248

Kč

/

Brožovaná

248

Kč

/

Brožovaná

1 121

Kč

/

Brožovaná

1 121

Kč

/

Brožovaná

365

Kč

/

Brožovaná

365

Kč

Knižní rádce Libroamiko

Užíváním tohoto chatu komunikujete s generativní umělou inteligencí. Jeho užíváním také souhlasíte se zpracováním osobních údajů.

Ahoj! Jsem Libroamiko, tvůj knižní rádce.

Jak ti můžu pomoct?

Ahoj, jsem Libroamiko, můžu pomoct?