Doprava zdarma při nákupu nad 1 499 Kč přes Zásilkovnu nebo PPL Box.

Staňte se součástí komunity milovníků knih z celého světa a získejte hromadu výhod.

Založit účet zdarma

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Kurýr DPD 69 Kč

PPL shop 49 Kč

Balíkovna 69 Kč

PPL kurýr 74 Kč

PPL box 39 Kč

Balíkovna 49 Kč

Výdejní místo DPD 49 Kč

Zásilkovna 39 Kč

Kontakt

Kontakt Jak nakupovat

Jak nakupovat

Pomoc

Doručení

Kurýr DPD 69 Kč

PPL shop 49 Kč

Balíkovna 69 Kč

PPL kurýr 74 Kč

PPL box 39 Kč

Balíkovna 49 Kč

Výdejní místo DPD 49 Kč

Zásilkovna 39 Kč

Doprava zdarma se Zásilkovnou nad 1 499 Kč

Nákupní rádce

Jsme tu pro vás!

571 999 090

Můj účet

▸

Prázdný :-(

0

Doprava zdarma při nákupu nad 1 499 Kč přes Zásilkovnu nebo PPL Box.

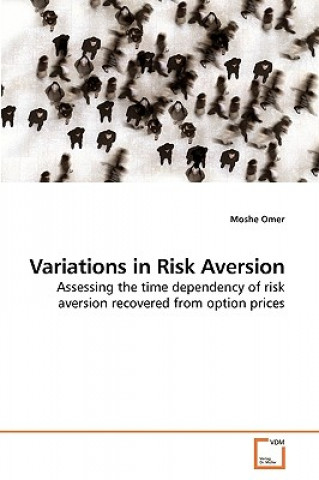

Variations in Risk Aversion

Assessing the time dependency of risk aversion recovered from option prices

Jazyk

Angličtina

Angličtina

Angličtina

Kniha

Brožovaná

In this paper recent techniques for recovering information implied by options market prices and real...

Celý popis

Libristo kód: 06828509

?

121 b

121 b

121 b

1 209

Kč

U nakladatele na objednávku

Odesíláme za 17-27 dnů

Až 30 dní na vrácení zboží

Zákazníci také koupili

/

/

Brožovaná

Brožovaná

1 451

Kč

1 451

Kč

/

Brožovaná

349

Kč

/

Brožovaná

349

Kč

/

Brožovaná

369

Kč

/

Brožovaná

369

Kč

In this paper recent techniques for recovering information implied by options market prices and realized returns are applied empirically to measure the risk aversion of investors in the Israeli stock market. We determine nonparametric volatility smile, densities and risk aversion functions from a ten years sample of daily option and stock market prices. Moreover, we construct a time series of the absolute risk aversion, and study its variation over time. We report decreasing and generally positive risk aversion function, which varies substantially over time and is negatively correlated with the ATM implied volatility.

Herečka

&

Polyglotka

EWA KASP

pro

Přehrát video

Libristo má největší výběr cizojazyčné literatury. Proto své knihy kupuji tady.

Informace o knize

Plný název

Variations in Risk Aversion

Autor

Moshe Omer

Jazyk

Angličtina

Angličtina

Vazba

Kniha - Brožovaná

Datum vydání

2009

Počet stran

52

EAN

9783639205343

ISBN

3639205340

Libristo kód

06828509

Nakladatelství

VDM Verlag

Váha

91

Rozměry

152 x 229 x 3

Darujte tuto knihu ještě dnes

Je to snadné

1 Přidejte knihu do košíku a zvolte doručit jako dárek 2 Obratem vám zašleme poukaz 3 Kniha dorazí na adresu obdarovanéhoMohlo by vás také zajímat

/

Brožovaná

671

Kč

/

Brožovaná

671

Kč

Knižní rádce Libroamiko

Užíváním tohoto chatu komunikujete s generativní umělou inteligencí. Jeho užíváním také souhlasíte se zpracováním osobních údajů.

Ahoj! Jsem Libroamiko, tvůj knižní rádce.

Jak ti můžu pomoct?

Ahoj, jsem Libroamiko, můžu pomoct?